A leaking roof, a sinking foundation — these issues are about as urgent as a house fire. Hopefully you never have to encounter such problems as a homeowner. But when it comes to the smaller things, where should your priorities lie? What fixes should happen first? Where should you focus your attention when nothing is *that* wrong?

The answers lie straight ahead. We’ve got the rundown, renovation order of operations that you’re looking for.

Know Before You Buy

Before buying a house, a home inspection should tell you exactly where some of the problem areas lie.

Keep a running record or write in a calendar when you’ll need to fix these issues. Make sure you address the issues before they truly become a problem. For example, if the water heater is 6 years old, know that you have between 2 to 6 yearsleft before you’ll need to replace it. You can start budgeting for these fixes now instead of getting slammed with financial surprises later.

General Replacement Timeline

Wondering how often you need to repaint the walls or when to repoint your brick? Let this renovation table serve as a guide:

Home Task

Redo or Replace Every…

Painting walls

5-7 years

Painting home exterior

5-10 years

Tuckpoint or repoint brick

25-50 years, more often in wetter climates

Repipe plumbing

Copper pipes: 70-80 years Brass & steel pipes: 80-100 years

Redo insulation

80 years

Replace vinyl siding

40 years

Replace roof

20-30 years

Here’s another guide on when to replace basic appliances (assuming that your appliance doesn’t die and need replacing sooner).

Home Appliance

Life Expectancy

Water heater

10-15 years, 15-20 years if tankless

Dishwasher

7-12 years

Oven

15 years

Refrigerator

14-20 years

Washer and dryer

12-18 years (dryers usually last longer)

Aesthetic Changes

What if you just want to redo some things around your house, solely for aesthetic purposes?

While you can technically replace certain things whenever, you should try to time things around other changes. For the sake of color coordinating, for example, you might want to hold off on updating kitchen fixtures until you need new appliances.

That being said, if you’re up to date on your home improvement list, nothing major needs replacing, and you’re hankering to finally add some backsplash and update your shower, go for it! Aesthetic changes add a ton to your home’s value — sometimes they are just as important as functional changes.

How to Keep Track

Keeping track of your home’s changes and renovations is critical. Not only does it remind you of when things were replaced or renovated, but it also helps inform future buyers and get the best value for your home.

One of the best ways to keep track is to create a spreadsheet documenting changes. It’s also a good idea to keep receipts or reports as well. However, you can make tracking changes into a fun project: for those with huge renovations underway, a scrapbook is a great way to show off your hard work!

Feeling inspired to make your home the very best? Want to start buying and flipping houses? Proud of your home’s progress but feeling ready to sell and start anew? Work with RealtyHive! From buying to selling, our time-limited events can do it all.

https://blog.realtyhive.com/wp-content/uploads/2020/01/umanoide-8NvFlA8DO6Q-unsplash-1-scaled.jpg11522048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2020-01-06 01:49:332020-05-19 21:26:49Home Improvement List: Order of Operations

Thinking of making a career change? If being your own boss, seeing beautiful homes, and helping people achieve their dreams sounds great, becoming a real estate agent should be in your cards. Take a look at the process, pros and cons of agent life to see if it’s the right career move for you.

Every state has different requirements. It’s important to see what’s expected of you before diving in. Keep in mind, you can become licensed in multiple states as well.

Take a prelicensing course.

Find a school with a good reputation and an equally good track record for post-graduates.

Apply for your real estate salesperson exam.

Each state has specific rules on whenyou can take this exam and whether or not you qualify. Some states require background checks and fingerprints which take awhile to process — know what you need to submit far in advance before you actually are ready to take the test.

Pass the exam

Hopefully you’ve studied and feel confident for your exam, but it’s OK if you don’t pass it the first time — you can retake it.

Find a broker.

Every agent legally needs a broker. Even though agents can also become real estate brokers, it’s best to interview multiple brokers and find one to work with (especially when you’re just starting out). After a sale, you will pay this broker through something called “commission splits.”

The Pros of Becoming a Real Estate Agent

You’re an independent contractor. You get to set your own rules! Take vacations when you want, work when you like — you set the pace for your work.

You get to work with others. Becoming an agent is a great job for anyone who loves working with people. While challenging, it is insanely rewarding to help people fulfill their dreams of owning a home.

You learn a ton of valuable knowledge. Knowing the ins and outs of real estate is immensely helpful when you’re looking to buy or sell your home.

You don’t need to go to college. While you have to take a prelicensing course, it’s much less expensive than paying for tuition. The course cost ranges by state but is usually $500 to $2,000.

You can start at the age of 18 or 19. Most decent paying jobs are unavailable to the youngest adults, but that’s not the case with agents. As long as you’re an adult who is also a legal resident, you hit the basic criteria for becoming an agent (though, as mentioned, you might have to also pass a background check, depending on state).

The Cons of Becoming a Real Estate Agent

Before diving in, we’d just like to point out that many of these “cons” could also serve as “pros,” depending on the person and the situation.

You won’t have any benefits. While there are some definite advantages to becoming an independent contractor, one of the biggest downsides is not having benefits. You’ll have to provide your own health insurance and set up a retirement fund.

You’ll need a solid network. If socializing and networking are your cup of tea, this isn’t a negative. However, you will struggle as an agent if this isn’t the case. Those living in rural areas or who just moved to a new city will definitely have an uphill (though not impossible) battle.

You probably won’t make as much as you think. At least, not at first. In fact, the median annual salary for a Realtor with 2 or fewer years of experience is $9,300. This leads us to our next point:

Most people aren’t full-time agents. Again, this isn’t necessarily a negative, but whether it’s because of the work, the time, or the lack of income (or all three), most people do other work on top of being an agent. It’s important to note that many agents don’t re-up their license once it expires for the first time (after five years).

While there are both pros and cons to becoming a Realtor, don’t let the negatives discourage you! RealtyHive works with agents, buyers and sellers alike. We can help you stand out in your market, differentiate from the competition and sell more properties. Become a member, market your properties, or represent a buyer with RH.

https://blog.realtyhive.com/wp-content/uploads/2019/12/business-woman-with-ipad-and-stylus-scaled.jpg13662048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-12-30 01:15:012023-04-19 16:37:41How to Become a Real Estate Agent

When it comes to selling or buying a house, everyone knows about real estate agents. Many people know about house offers and contingencies, and even more people know about the need for homeowner’s insurance. But there’s one very crucial element to real estate that remains somewhat of a hazy mystery:

What exactly is a title company?

What is a title?

Before buying a house from someone, you need to make sure that they legally own the property. A title company does just that. They run a search to ensure that, before a sale goes through, the current homeowners legally own the home.

People sometimes confuse titles with deeds:

A deed is a legal document that transfers the property between owners.

A title is a legal document that states who owns the property. When you become the new homeowner, the title is now in your name — sort of like registering your car.

When is a property legally owned?

A property that’s owned free and clear has no mortgages or liens associated (the house is paid off). However, you can still sell a house when you have a mortgage.

In this event, you’ll give your money to a middle man (usually the title company that holds the escrow) and they’ll pay off the seller’s mortgage. The proceeds will then roll into a new property, their bank account, etc.

Here are some instances where a property might not be legally owned:

Unpaid taxes

Outstanding mortgages (mortgages that weren’t previously discussed)

Illegal boundaries or encroachments

Ex: A house that is not entirely on the land that it’s zoned/surveyed for (such as a house that’s partially built on a neighbor’s land) would bring up issues.

Restrictions, leases, or easements: A person can still legally own a property with any of these, but they must be disclosed to the buyers.

Problems with the deed

Ex: The previous sellers bought the house from someone in their family or in some other “under the table” format but there is no deed to prove they own the house.

Every homeowner needs title insurance.

The last thing you want is to buy a house with a legal issue. If that happens, the problems of the past homeowners become your problems unless you have title insurance.

Title insurance protects you in case the home you’re planning on buying is not legally owned.

Title company ≠ title agency.

A titleagency represents the title company; the title company itself underwrites and distributes title insurance. When you close on a house, you’ll most likely meet with a title agency (and you can choose which agency you work with).

Can title companies get something wrong?

It’s scary to think about but it’s true nonetheless: sometimes title companies make mistakes.

In all honesty, many times what might seem like a mistake is actually a lack of comprehension or understanding on the part of the buyer or seller. This is why it’s essential to have a lawyer or real estate agent with you to go through the closing paperwork.

However, when a title company truly is at fault, they are liable. Be sure to carefully look over everything before signing and again, bring a lawyer with you.

Will title companies continue to play such a vital role in the future?

It’s more than likely, but the paperwork part might change. Instead of printing massive amounts of paper for reading over and signing, there’s a chance that title agencies will go paperless in the future. Cook County (where Chicago, IL is located) uses blockchain for closing transactions, eliminating paper.

Whether you’re a seasoned vet or complete novice in the real estate industry, RealtyHive has the resources you need. Sift through our listings to find a home near you (and get cash back with Cashifyd), sell with a time-limited event, or browse through our blogs for the latest in real estate info.

https://blog.realtyhive.com/wp-content/uploads/2019/12/helloquence-5fNmWej4tAA-unsplash-1-scaled.jpg13672048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-12-17 01:03:202020-05-19 21:29:18What Exactly Is a Title Company?

Congratulations! You’re pretty sure you’re ready to buy a house. You’ve done some research and you’ve been scoping out houses available in your area online. Great! So what comes next?

Buying a home is a REALLY big step — probably the biggest financial move you’ll make — and it can come with a lot of anxiety and questions. Luckily, here at RealtyHive, this is something we do Every. Single. Day. Here’s a REALLY simplified version of the home buying process in a perfect, simplea(and often typical) transaction.

1) Get Pre-Approved

Before you even think about talking to an agent, you’ll want to talk to a few mortgage lenders about what you’re looking for and what you can afford. It’s a good idea to talk to at least three different lenders: one from a bank, one from a credit union, and one from a mortgage lending institute. This is one of the biggest steps in the process so it’s a good idea to have a little background before you set these meetings up. Check out Home Loans 101 to learn everything you were never taught about home loans in school.

2) Find an Agent

There’s often a debate on whether or not you need to use an agent when selling a home, but when it comes to buying, the answer is clear. You need to use an agent. Among the other benefits (Check out this article on why you need a Buyer’s agent), you won’t pay anything for their services and they’ll guide you along during the process.

BONUS: RealtyHive has a new program called Cashifyd that pairs you with a local agent who will show you homes, give you advice, and give you a cash back credit on your closing costs (saving you money)!

3) Find Contender Properties

Your agent will likely set you up with a listing cart from their MLS (an agent-only portal that shows the info on all available properties in your area). You’ll be able to set filters like number of bedrooms, bathrooms, size, location, and others to narrow down your selections. If you’re interested in possibly seeing “For Sale by Owner” properties, it’s a good idea to keep an eye out for those as they won’t show in your listing cart. When you find a property you want to see, tell your agent and they’ll set up a showing for you.

4) Visit Properties & Fall in Love

Depending where you live and where you’re looking to buy, the market could have a plethora of properties that meet your criteria or you may be looking for awhile. If you find “the one” right away, great!, but don’t feel obligatedto write an offer on a home you’re not completely sure of just because you’ve been looking for awhile. It’s important to remember that things like landscaping and paint colors can be changed easily, but major repairs and permanent features (like location) are deciding factors.

5) Make Your Offer

Again, depending where you are and what you’re looking at, you might be the only offer the property receives or you may be one of several offers. This is where having an agent is vital. They can help you make a compelling offer and make sure you include the things that are important to you (like having inspections). You’ll sit down with them and complete the multi-page offer that covers everything from purchase price (including earnest money) to contingenciesto timelines.

5) Offer is Accepted

In the best case scenario, your offer is accepted outright. It could also be rejected or the sellers could counter your offer to try to get a more amicable deal. Assuming the offer is accepted, you are now one (major!) step closer to being a homeowner.

6) Get Your Checkbook Ready

From this point on, things move pretty quickly. First you’ll need to submit your earnest money. This is a like a downpayment to the seller that says “I’m serious enough to put this down” Your earnest money will come back to you as a credit on the closing statement or refunded to you if the deal falls apart due to contingencies outlined in your offer, but be aware that you could lose your earnest money if you back out of the deal for no good reason.

7) Get on the Phone

While you’re basking in the excitement of your accepted offer, there’s a few things you need to accomplish. First, you’ll need to talk to your insurance agent. You need to prove that the home is insurable and they can get the paperwork rolling on that. They’ll need to provide this to your mortgage lender and you’ll have to pay one year of homeowners insurance before closing. The next thing you’ll (most likely) need to do is schedule inspections. Depending on what type of inspections your wrote into your offer, you could be looking at scheduling a few different inspection ranging from a general home inspection to a well and septic test to a radon test. You’ll want these to be scheduled as quickly as possible so that you don’t miss any of the following deadlines (which could cause the deal to fall apart). You’ll also let you lender know that you found a home and have an accepted offer, but be sure to tell them to NOT schedule the appraisal if you’re waiting on inspections. Also during this time a floodplain check will be done by the lender. This is to ensure that the home is not in a floodplain area and you can often get out of your offer if you do not like the results of this check.

8) Have the Lender Schedule Appraisal

If you’ve got your inspections done and you’re still wanting to proceed with the purchase, it’s time to let your lender know to schedule the appraisal. This inspection is a little different than the inspections you just had done. You can learn more about appraisals in Appraisal, Assessments, and Inspections.

9) Money, Money, Money

When the property appraisal comes back at or above the purchase price, it’s loan commitment time. There’s nothing you need to do here, but you should be aware that this is going on. Shortly after this, your lender will let you know exactly how much money you need to bring to closing. Be aware that there are costs outside of whatever you offered on the property that you will be responsible for. These can include tax escrow, title fees, appraisal fees, and more.

10) Final Walk Through

A day or a few days before closing, you’ll get your chance for a final walkthrough. This is your last chance to make sure everything is in (roughly) the same condition as when you put in your offer. Keep in mind that minor wear and tear can happen and that if you’re planning on getting out of your offer at this time, you should have a really good reason or you’ll almost certainly be forfeiting your earnest money.

11) Closing Time

On closing day, you’ll meet with your agent, your lender and the representative of the title company to sign papers. You’ll give them the closing cost money (your lender will provide the mortgaged amount) and sign many papers. After that you’ll get the keys.

Congratulations, you are now a homeowner!

Simple, right?! Let us know of any questions you have in the comments section below or check out some of the amazing properties for sale now on RealtyHive!

https://blog.realtyhive.com/wp-content/uploads/2019/12/AdobeStock_16789283.jpeg13652048Tristin Zemanhttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngTristin Zeman2019-12-04 19:29:432020-05-19 21:31:05How to Buy a House: A Beginner's Guide

Ever heard of a reverse mortgage? It’s a murky term for most folks (even homeowners). Take a look at this lending option (and whether or not it’s a good idea).

What is a reverse mortgage?

In a traditional mortgage, you’ll take a loan from the bank to pay for your house, and will pay the bank back in monthly payments.

Eliminates existing mortgage — the money remaining on the mortgage is yours to use however you like.

Instead of making monthly loan payments, the loan’s interest is applied to your reverse mortgage.

When it’s due, you pay all at once, either by selling your house or paying for it outright.

A reverse mortgage is due either when a borrower sells their house, passes away, or lives outside their house for a year.

Your family can keep the home by paying off your loan balance or paying 95% of the home’s value.

Why do people get a reverse mortgage?

The biggest reason people take out a reverse mortgage is to gain capital for retirement purposes. People are staying in their homes longer than ever before and spending more time in retirement as a result. Taking out extra equity from your home can supplement retirement, but not without a cost.

How long does a reverse mortgage last?

Unlike a typical 30-year mortgage, there’s no set term for a reverse mortgage. The mortgage must be repaid when a borrower moves out of their house for a year, sells the house, or passes away. The average time of repayment is 7 years, but again, this varies for every borrower.

What are the risks of a reverse mortgage?

There are quite a few. It might sound great to get a bunch of cash upfront, but paying off the reverse mortgage either requires selling your house or paying for your home’s value all at once years down the road.

Oftentimes, a reverse mortgage hits the borrower’s family members the hardest. When a borrower passes away or the loan is due, their family will need to pay for the loan or deal with selling the house. A reverse mortgage is a bit of a “pay the consequences later” financial decision.

Not to mention, reverse mortgages have unfortunately received an unsavory reputation. For decades, this type of loan preyed on the elderly (an already vulnerable population) by saying this was an easy way to get more money and still live in their home.

Many people bought into this concept without understanding how much they would have to pay back later on. If a sudden health issue forces a homeowner to an assisted living community, the loan will need to be repaid in 12 months — not leaving anything for bills.

Is a reverse mortgage ever a good idea?

The answer is different for every person, but there are a few situations in which it could work. If a homeowner is set on selling their home and there is zero chance they’ll live anywhere but their home until they pass away, they could take advantage of that equity in the meantime.

Is it possible to owe more on a reverse mortgage than what a home is worth?

Only if the reverse mortgage is not federally insured. As long as it’s federally insured, a homeowner never pays more than the value of the home — the FHA covers the difference.

While a reverse mortgage is an option, you might have a better time selling your home and downsizing. If that’s the case, RealtyHive is here to help. Check out our properties for sale and secure your finances without having to take out a reverse mortgage.

https://blog.realtyhive.com/wp-content/uploads/2019/11/frankie-valentine-WWS9i5_Q8vE-unsplash-1-1-scaled.jpg16372048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-11-15 23:34:292020-05-22 19:53:08What Is a Reverse Mortgage (And Is It a Good Idea)?

Whether buying or selling your home, you want to get the best possible deal. A real estate auction is an amazing and innovative way to do that. But between Concierge Auctions and RealtyHive, which is the better real estate auction company?

It might seem counterintuitive to write about our competition but ultimately, we want every buyer or seller to feel confident in the company they choose. Read on as we weigh out your home auction options.

RealQuick: What are real estate auction companies?

You might have an idea just from perusing our site, but we’re happy to break things down for any first-time guests (welcome, by the way!). A real estate auction company works with sellers, buyers, and real estate agents to help a home sell at a live auction (sometimes called a time-limited event).

Feel free to look through our buying and selling pages to find even more benefits, but at the very least, hopefully you better understand what a real estate auction company does.

How RealtyHive and Concierge Auctions Are Similar

Purchasing Time Frame

For both real estate auction companies, buyers can purchase a property at or before the event.

International Exposure

International properties are available for purchase (and can be sold) through RealtyHive and Concierge Auctions.

Reputation and Success

RealtyHive and Concierge Auctions both have pretty solid reputations and proven industry success.

How RealtyHive and Concierge Auctions Are Different

High Fees

Concierge Auctions has a successful track record just like RealtyHive, but it comes at a price. They charge much higher fees than our real estate auction company — 12% or a minimum of $175,000. This might give you a clue into our next point…

High-End, Luxury Properties

We at RealtyHive are all for high-end properties (like this condo in the Bahamas), but we also offer plenty of more modest homes. Concierge Auctions solely accepts super luxurious properties. At RealtyHive, you don’t have to be a multimillionaire in order to find (or sell) a home.

Real Estate Agents

Concierge Auctions do not deal with FSBO sellers — you must work with a real estate agent with them. At RealtyHive, you don’t need an agent if you don’t want one. But if you want one, that’s great too! We’ll draw on our amazing network of agents to find you the perfect person.

We’re proud of the qualities we share with Concierge Auctions, but we’re perhaps even more proud of what sets us apart. Whether you’re looking for your dream home or feeling ready to sell your current one, set yourself up for real estate success with RealtyHive!

https://blog.realtyhive.com/wp-content/uploads/2019/11/Untitled-design.png6751200Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-11-14 01:37:102023-04-18 13:41:56RealtyHive vs. Concierge Auctions

We’ve talked about how you can make money in real estate, but what are some ways this investment can backfire? By knowing how people can lose money in real estate, you’ll be better prepared to make a good investment.

Market Downturns

This is one of the most well-known ways of how a good home purchase can turn into a bad real estate investment. The impacts of the 2008 housing market crash are still felt by many today.

The good news is that a housing bubble and subsequent bursts can be tracked. There are no guarantees, but even in the years leading up to 2008’s crash, many people were already nervous about where home prices were headed. Read up and stay informed on the state of the housing market to help make good real estate investments.

Bad Neighbors

While you might be able to put up with the Urkels and Kramers of the world, future buyers probably won’t. From nearby factories to neighbors who care little for their curb appeal, bad neighbors can negatively impact your home sale.

Bad History

A death in your house — even if occurring naturally, and even if from a previous owner — spooks people from wanting to buy. Unfortunately, there are enough horror movies to scare potential buyers from wanting a home with some, erm, history.

Going Over the Top

Rapper 50 Cent had to take around an 80% cut on his mansion. Michael Jordan still hasn’t sold his Chicago home. The more over-the-top your place, the more niche your buying market becomes. This inevitably lessens your chances of selling.

Some personalized details to your home are OK, but there’s a fine line between “unique” and “eccentric.” Before making any substantial changes, remember to think with a seller’s mindset — you won’t own this home forever.

Too ________

Too big, too much carpet, too many cobwebs, too little closet space, etc. Buyers are like Goldilocks — they want a property that’s juuuust right. Keep up on current trends to know what buyers are looking for.

And remember — if there are things that bother you about your property, they’ll likely bother others. It’s better to make those changes now and increase your home’s value when it’s time to sell.

If you’re reading this list and wailing at all the boxes your home checks, don’t despair! RealtyHive offers time-limited events to make selling easier. Even if you’re ready to get rid of your home as-is, we’re the ones to call. Sell with RealtyHive for a stress-free process.

https://blog.realtyhive.com/wp-content/uploads/2019/10/daniel-barnes-RKdLlTyjm5g-unsplash-2-scaled.jpg11512048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-10-15 01:16:372020-05-22 19:59:22How to Lose Money in Real Estate

It’s tough and competitive to be a real estate agent. In most states, agents try to set themselves apart from their competition by offering real estate rebates to potential homebuyers. Find out how rebates work, and how our new Cashifyd app can help buyers and sellers alike.

What are real estate rebates?

Real estate rebates are incentives, usually monetary in some way, that agents offer homebuyers who choose to work with them. This might be cash back after closing (usually up to 1% back from the broker), a gift card, or some other type of gift.

Are rebates hurting consumers?

The Justice Department did a study on this very topic. They found that rebates are actually helping consumers because it’s saving them money on such a huge investment. Even a little bit of savings can go a long way.

Can anyone get a real estate rebate?

No. There are nine states that do not permit rebates. Rebates are prohibited in Alabama, Alaska, Kansas, Louisiana, Mississippi, Missouri, Oklahoma, Oregon, and Tennessee. Iowa doesn’t allow rebates when two or more brokers are used

Traditionally, rebates are only for homebuyers. Sellers have to pay commission for real estate agents, so they could try to negotiate paying a lower commission. But this isn’t exactly a rebate or incentive for sellers — they’re just paying less money.

However, rebates are about to change and include sellers as well. That’s because RealtyHive is introducing Cashifyd, the only app that allows buyers and sellers to get cash back on a home sale.

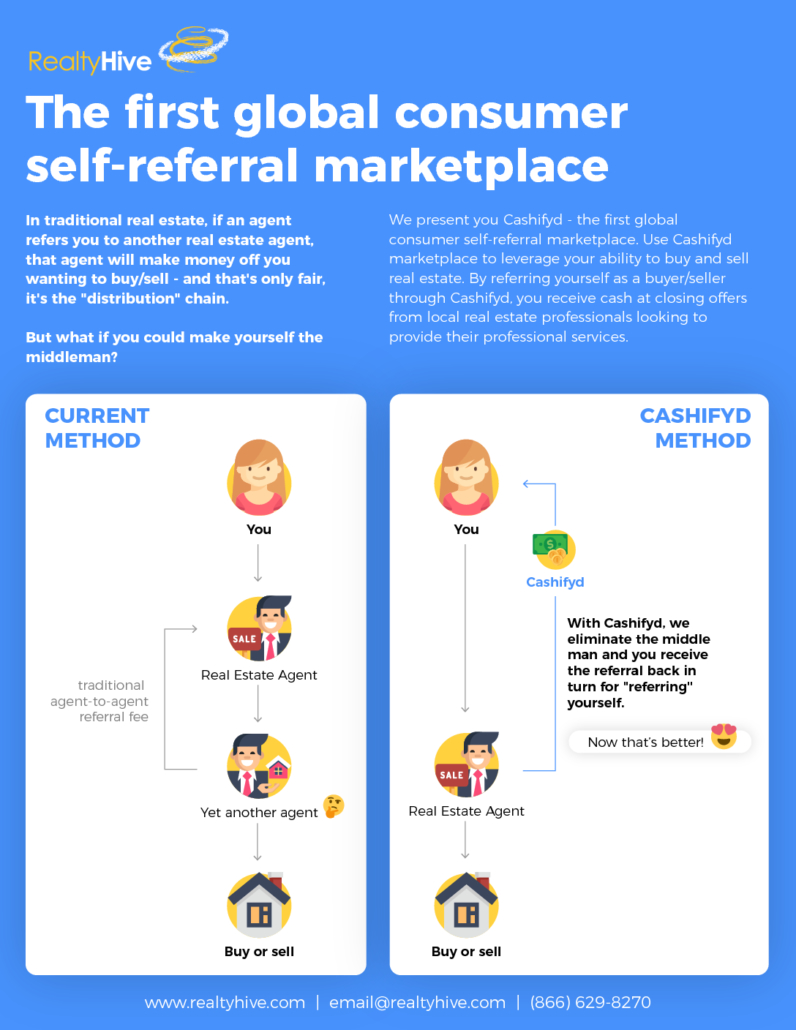

Make Yourself the Middleman With Cashifyd

Cashifyd is a self-referral marketplace — the first and only of its kind.

If you are a seller looking for an agent, you’ll still pay for their commission. The difference is that by looking for agents through Cashifyd, you’ll actually get money back.

If you’re a buyer looking for an agent, you’ll receive a referral rebate when working with Cashifyd.

If you’re an agent on Cashifyd, you only pay referral fees when sales happen. No more having to pay big real estate databases for leads that lead nowhere.

How do Cashifyd rebates work?

Other real estate rebate programs have it where you only get cash back if it’s a house that a particular site or company is selling (or helping you buy). In other instances, you might only get a rebate by working with a specific agent.

With Cashifyd, rebates apply for any property and almost any agent — we say “almost” only because the agent has to agree to partake in this. But as of this blog post, we haven’t had anyone say no!

Cashifyd rebates do not work in those aforementioned nine states, but otherwise can be used around the world. Even buying an international property could land you a referral rebate! And as mentioned, this is the only option for sellers to get a rebate, too.

RealtyHive strives to make buying and selling a better experience for all. Get ready for the Cashifyd launch, and start saving money on your next home sale or investment!

https://blog.realtyhive.com/wp-content/uploads/2019/09/cropped-sabine-peters-ouGoHu6Ow7w-unsplash-1-1.jpg11552048Emily Wottrenghttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngEmily Wottreng2019-09-17 01:28:202023-06-26 10:04:15Rebates for Homebuyers (And Sellers!)

5 things agents can’t tell you (and how to find out yourself)

Using a real estate agent is a great way to avoid many of the headaches (and potential heartaches!) associated with buying or selling a home. As part of their services they can help you appropriately price your home, negotiate on your behalf, and their access to an MLS –an exclusive network of property listings– can help you sell your home or find the right one before the general public ever sees it. But, as licensed professionals, there are some things that your agent can’t tell you.

Not won’t tell you, but legally or ethically, I’m-sorry-but-I-really-cannot-tell-you.

Now that doesn’t mean you’re on your own and just have to hope for the best, though. For that information, you’re going to have to do some of the digging yourself. Here are the 5 surprising things your real estate agent can’t tell you.

“This area is great for young families!”

This one seems so innocent and well-intentioned, but is actually illegal! Maybe you passed a park on the way to the home or noticed the nearby elementary school, but whether you’re looking to live in an area where your kids can roam with the neighbors or you’re trying to avoid children altogether, your agent isn’t allowed to tell you who lives in the area.

Reasoning: Under the 1968 Fair Housing Act, family structure is a protected class meaning a comment like this could dissuade older couples or a single party from the property, making it illegal.

How to find your answers: If driving through the area isn’t an option, Google maps is one of the best tools for doing neighborhood recon. Simply type in the address of the property you’re looking at and check out the area you’re interested in. Are there parks and schools nearby or is it in a more industrial area? Is the area filled with side streets and cul de sacs or is it on one of the main roads? Depending on what you’re looking for you may want to switch your search based on what you see.

“You don’t want to live in that area. That’s where the [nationality, gender, age group] live!”

In addition to not telling you where to live based on the demographics, your agent also cannot tell you not to live somewhere because of the people in the neighborhood.

Reasoning: As mentioned above, the Fair Housing Act prevents any discriminatory statements based on protected classes.

How to find your answers: You can find out more about the general demographics of an area by checking out the US Census Bureau’s website. This tool, with most recent studies being from 2016 can tell you the age, sex, and race of the population down to a zip code level.

“Are you sure you’re interested in that area? It’s pretty high crime.”

While you might think that an agent saying this is just looking out for you, this is another no-no statement. Crime statistics are public information, but because crime rates often lead to conclusions about the racial makeup of an area, your agent is best protected by letting you find your own conclusions.

Reasoning: Race is a protected class under the Fair Housing Act and whether it’s the intention or not, discussing the crime rate of a particular area could lead to assumptions about the racial makeup of that area.

How to find your answers: If finding out about crime in an area is of particular interest to you there are plenty of free sources to look. The National Sex Offender Public Website (NSOPW) offers a location-based lookup that links the data from public state, territorial, and tribal sex offender websites. To find incident-level crime lookup, you may have to check a couple of website as not every jurisdiction reports to every available site. Here are some good ones to start with: MyNeighborhoodUpdate, CrimeReports, SpotCrime, and NeighborhoodWatchDog. You can also check the website of the local police station as they may provide a link to the crime mapping site they use.

Buying home is an emotional time. It’s a big investment with a lot on the line, but having an agent you trust can make all the difference. Ready to take the leap and connect with a top agent? Check out Cashifyd, a program offered by RealtyHive that connects you with top local agents who offer cash back incentives when you buy or sell your home.

https://blog.realtyhive.com/wp-content/uploads/2018/01/agent.jpg640960Tristin Zemanhttp://blog.realtyhive.com/wp-content/uploads/2018/08/RealtyHive_Horizontal_white_no_shadow.pngTristin Zeman2018-01-17 15:56:262023-06-26 09:17:26Things Your Real Estate Agent Can't Tell You